More About Term Life Insurance

Level Term: The death benefit and premium stay exactly the same throughout the policy.

Decreasing Term: The death benefit gradually drops over time; it is often used to cover a debt that also decreases, such as a mortgage.

Increasing Term: The death benefit grows over time to keep pace with inflation or growing financial needs.

Annual Renewable Term (ART): A one-year policy that can be renewed each year, though premiums typically increase significantly as you age.

Common Types of Term Life Policies

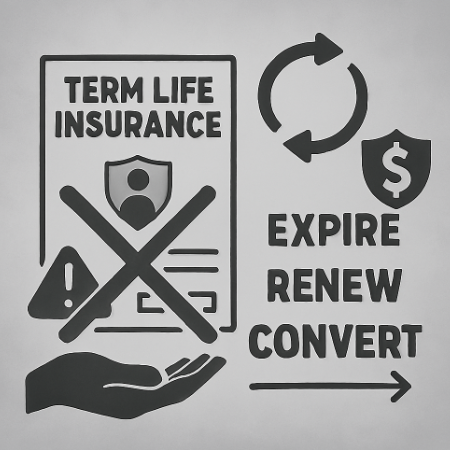

What Happens at the End of the Term?

When a policy expires, you generally have three options:

Let it Expire: The coverage ends and you receive no money back.

Renew: Many policies allow you to renew for another year or term without a new medical exam, though the cost will be much higher.

Convert: A "convertible" policy can be switched to a permanent life insurance policy without requiring a new medical exam, provided this is done before a specific deadline.

Term life is often recommended for people with temporary financial obligations. Examples include:

New Parents: To ensure their children are provided for until they reach adulthood.

Homeowners: To cover a 15- or 30-year mortgage.

Primary Breadwinners: To replace lost income during their peak working years until retirement.